What are Solo 401(k) Plans?

In a world where many embrace self-employment in their careers, the self-employed Roth 401k is an intimidating powerhouse for retirement planning. This financial instrument is designed quite purposely to assist owners, advisors, per diem workers, and self-employed gurus with no W-2 workers to share the business earnings. The appeal lies in its no-nonsense approach: you obtain virtually full flexibility over your retirement plan without assuming the legal responsibilities of an employer-sponsored retirement plan.

The concept of Solo 401(k) is slowly picking up because it shares the advantages of 401(k) while offering the simplicity that is desired by an individual running a business. As presented by higher contribution limits and giving tax deductions these plans provide a viable and sustainable solution for securing financial stability during retirement.

Why Every Self-Employed Person Should Have a Solo 401(k) Plan?

Having a retirement plan that essentially gets the fact that self-employment is different can be a massive advantage for the self-employed. This is an area where solo 401(k) plans particularly shine – mobile and highly customizable, it lets business owners steer their savings as they will. For this reason, the fact that there is no need for full-time employees makes the solo 401(k) plans highly attractive. Self-employment is not a uniform phenomenon and requires coverage that will be unique to the circumstances that are prevalent with everyone who is self-employed from time to time.

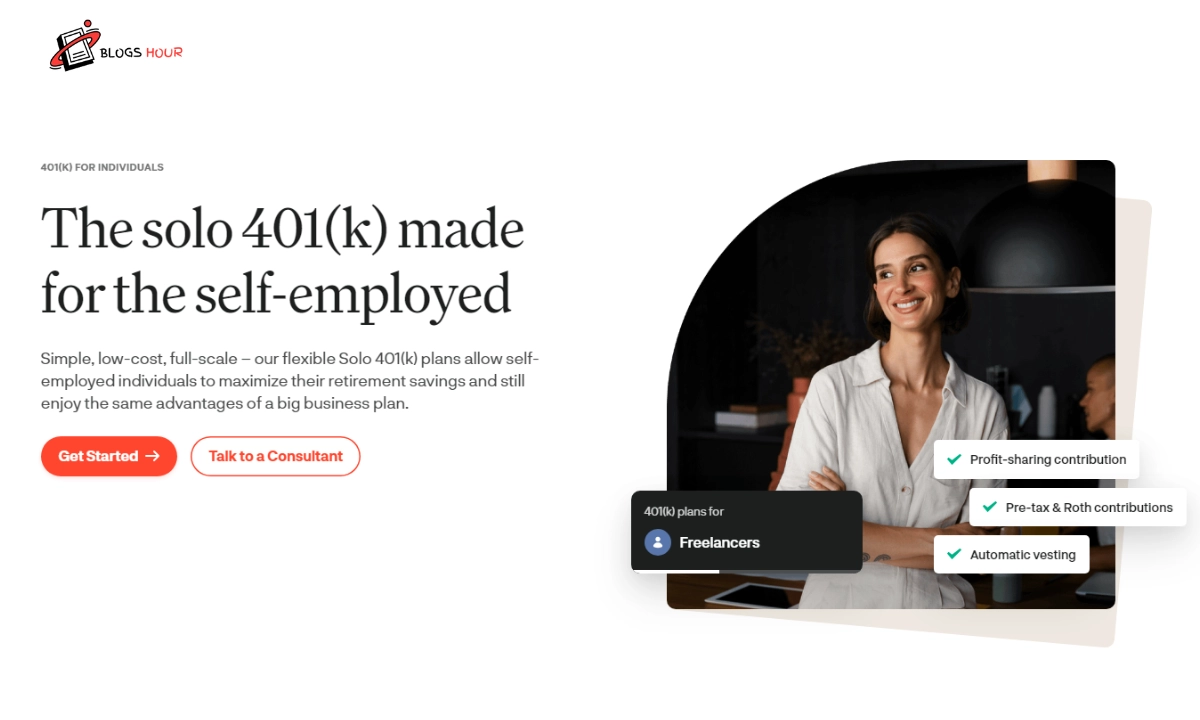

Imagine you’re a freelance graphic designer or consultant who wants the best of both worlds: These plans give you those lucrative contributions and strong tax shields – these are on a silver platter for you. The self-employed can enhance their savings substantially by making contributions as both, the employee and the employer.

Key Features of the Solo 401(k) Plans

Another interesting aspect about solo 401(k) plans one would want to note is the fact that there are many options you can avail to contribute. The features are that participants can contribute as both the employer and the employee at the same time, which is quite unusual in other SR vehicles. This feature helps you to get the most out of your contributions as per the federal rules and regulations on contributions.

In addition to contribution flexibility, 401(k) plans usually contain a loan provision. Employers can take loans against their plans meaning that they can have the liquidity they require without the normal early withdrawal penalties. A possibility to take loans can serve as the essential one in moments when the financial requirements increase or when new business promising opportunities appear.

Contribution Limits and Tax Advantages

These plans are famed for the fact that they have high contribution limits when compared to other types of retirement plans for self-employed workers. According to IRS guidelines participants in contributions are also capped at $66,000 per year while if the contributor is 50 years and above they get an extra contribution. This brings even more savings under the tax-advantage shield. These contributions can be pre-tax as well as after-tax and Roth investments for more flexibility in taxes.

This decision makes it control how much is contributed annually enabling the use of pre-tax contributions to minimize the amount of taxes paid at any one time. However, the contributions made to Roth can be made from pre-tax money, and those invested grow without the burden of tax to reduce the tax on distributions in retirement.

Comparing Solo 401(k) with Other Retirement Plans

Other structures like the SEP IRAs and SIMPLE birthday parties do exist as appreciation models of retirement saving especially for small businesspersons, but why 401(k) plans stand out as the better option are factors that are unique to the kind of opportunities they present to small business owners. With Solo 401(k) plans the contribution limit of the plans is higher than with SEP IRAs and unlike SIMPLE IRAs they offer the provision of taking a loan against your contributions.

The novelty of a solo 401(k) retirement plan coupled with its high degree of freedom, and convenient loan opportunities make it a worthy rival to conventional retirement plans. This flexibility can be essential for independent contractors who require money on short notice without large penalties.

How to Establishing a Solo 401(K)

Forming a solo 401(k) plan may seem complicated at first, but once one knows what to do it is quite easy. To begin with, enroll with a reliable and experienced financial institution in the offering of Solo 401(k) plans. Resources such as the Fidelity guide should be used to make the setup process more effective based on your financial plan and business form.

Once your provider is selected, you have to fill out a questionnaire that gives information on your business and your planned donation. Once you are ready to set your financial plan up, most institutions will offer guidance and assistance as well as explain whether the structure of your plan conforms to the IRS’ standards and your business model.

Some of the Misconceptions About Solo 401(k) Plans

Some myths concerning solo 401(k) prevent numerous individuals from looking into this high-impact retirement savings vehicle. One common stereotype is that the program is elaborate in terms of implementation and administration of the 401(k). Most people believe it is much more complex than simple 401(k) schemes. But this is a misconception people have.

By providing the right information and access to the implementation process, the creation of a solo 401(k) is not much different from putting up a conventional 401(k) plan. This is because such plans are specifically designed for individuals, particularly independent contractors and small company owners, meaning that every person’s finances and goals may also be unique, resulting in a more personal, and potentially, more efficient retirement savings plan.

The second major misunderstanding that people have is the idea that it ties your money up and does not allow you the freedom that may be afforded by other kinds of retirement savings plans. This is the opposite of what some people have said about solo 401(k) plans being rigid with several constraints which may not be far from the truth. For instance, they provide for differential contributions, whereby both, salaries and profits, can be matured and contribute in different proportions, and vary annually depending on the performance of the business.

Moreover, these plans also give the participant the privileges of a loan against the balance in the account, providing flexibility in tough economic conditions. A level of flexibility in this way ensures people may as early as possible change their retirement savings plan according to changes in their financial situation, for instance, resulting from alteration of their personal or career status.